Abstract

There is a demand for clean and green energy around the world and Nepal has a huge potential for the production of hydel electricity. According to estimates by an ADB study in 2020, the technical and economically feasible hydropower potential of Nepal has been estimated at 83,000 and 42,000 megawatts (MW), respectively. However, Nepal is heavily dependent on external financing for tapping or optimal utilization of its hydro-potential. In 2019, Nepal updated its Foreign Investment and Technology Transfer Act (FITTA) to attract more FDI and meet the financial gap between public investment and capital expenditure. It has been taking various investor-friendly measures to boost its economy ever since the new Constitution was adopted in 2015. Despite all this the overall economic performance of Nepal has not been satisfactory. This is reflected in the poor GDP growth, increase in labour migration due to the failure of the domestic market to absorb unemployed youths, rapid decrease in foreign currency reserves, failure of the banks to provide loans for big projects, widening trade deficit, and poor inflow of foreign investments. The present paper seeks to study the policies that Nepal has put in place and the challenges that it is facing in enabling a conducive environment for investment to bring about all round economic growth and development in the Himalayan country.

The climate change effects have redefined the significance of Himalayan green energy given the climate commitments of India and other South Asian countries to transit half of their economy from fossil fuel to green energy by 2030. India could be a US$ 30 trillion economy by 2050. As a result, its energy consumption would rise 400 percent by that time.[1] At the same time, India has to maintain a balance between improving the standard of living of its population and at the same time keeping the emission level low by transiting to green energy.[2]

India’s current installed power generation (both fossil and renewable) capacity is 4,03,760 MW. Of that fossil fuel contributes 58. 5 percent and 41.5 percent comes from renewable energy. India needs to reduce its dependence on fossil fuels by further nine percent to achieve its Paris Agreement by 2030. At the same time, it is important to note that India’s energy consumption would be doubled by 2032 from its current consumption.[3] In that case, India could increase its dependence on Nepal and Bhutan for hydroelectricity for meeting its energy needs and its climate commitments.

At the same time, Nepal wants to export its surplus electricity to other South Asian countries (Bangladesh and Myanmar) by using Indian transmission lines. With 42,000MW hydroelectricity Nepal could harness, the Himalayan country aspires to become the power hub of South Asia. In this regard, Nepal has been planning to construct additional cross-border transmission lines with India to export at least 13,000 MW of electricity to India in the next five years (By 2027).[4]

Nepal’s geo-economic profile has gone up with the emergence of India and China as the major economic powers in Asia. While India has been a major investor in Nepal since the 1950s, China has, of late, expanded its outreach in Nepal by investing in hydro-energy, as well as in services, tourism, and manufacturing sectors since 2010. In fact, China replaced India as the topmost investor in Nepal in 2013. By July 2014, Chinese investment had reached NPR 29.80 billion with 108 projects. In comparison, India pursued 18 projects with an investment of NPR 8.22 billion in that period.

In terms of diversity of foreign direct investment (FDI), 94 countries have invested in Nepal (in 2022). Among these countries, China has been the largest contributor followed by India, US, and South Korea (Industrial Statistics, 2022).[5] However, the cumulative FDI continues to be too small to help Nepal build an economy of scale. It is imperative to trace the policy options Nepal has chosen for itself over the years, especially since constitutional democracy was initiated in Nepal and the effect it has had on the overall financial climate in Nepal, critically analyse the reasons for continued apathy of the investors and suggest measures to overcome the challenges in the future.

In 2015, there was excitement and euphoria in Nepal after the adoption of the Constitution that the new document would finally put an end to some of the nagging decade-old problems like political instability, development deficit, and deprivation of the marginalized groups. The new Constitution, in fact, encourages partnerships between public, private, and cooperatives for enhancing the national economy.[6] In 2019, Nepal updated its Foreign Investment and Technology Transfer Act (FITTA) to attract more FDI and meet the financial gap between public investment and capital expenditure.

Despite all this, the overall economic performance of Nepal has not been satisfactory. This is reflected in the poor GDP growth, increase in labour migration due to failure of the domestic market to absorb unemployed youths, rapid decrease in foreign currency reserves, failure of the banks to provide loans for big projects, and widening trade deficit,[7] especially with India and China, skyrocketing inflation, and poor inflow of foreign investments.

According to World Bank, in 2021-2022, Nepal’s FDI inflow was the lowest in the region at 0.5 percent of GDP. In 2020, it was just 0.2 percent. While there was a marginal growth year on year, this can be increased through further easing of regulatory approval procedures, which may accelerate foreign currency inflows and stimulate growth through capital and technology transfers.

There was a time, until two years ago, Nepal did not have sufficient electricity to supply to its industries. Since July 2021, Nepal has been producing 2200 MW, including a surplus of 500 MW, which is being exported to India. As of November 2022, the Nepal Electricity Authority (NEA) witnessed reduced power demand in the country, particularly from the industrial sector, which indicated that the country’s economy was slowing down. Quoting Shekhar Golchha, president of the Federation of Nepalese Chambers of Commerce and Industry (FNCCI), a media report said industries were operating far below their capacity as they are struggling to get bank loans due to high-interest rates and lack of liquidity from banks. As per media reports, “except for factories related to FMCG [Fast Moving Consumer Goods] and food grains, production from others has come down by 50-70 percent. Firms producing construction materials such as iron and steel, the education sector, the automotive, consumer electronics, textile and garments, and insurance sectors are witnessing a slowdown”.[8] Others have suggested that this trend indicated “structural issues facing the economy” and held that production, “which is limited by insufficient private and public investment, must increase to increase export”. Investments in Nepal are hampered by poor performance of the following indicators: “prevailing tax policy, market size, availability of raw materials for manufacturing, wage rate, quality of technology, cost of transportation, and labour productivity”.[9]

Although many would argue that COVID-19 and the crises arising out of the ongoing Ukraine war were responsible for the dismal economic performance of Nepal, the situation was not quite optimistic before the unfolding of these two events, especially in the field of foreign investments, despite Nepal hosting multiple investment summits since 2017. Despite taking such measures, Nepal continued to receive a very low volume of FDI and what is even worse, many of the committed investments seldom materialized.

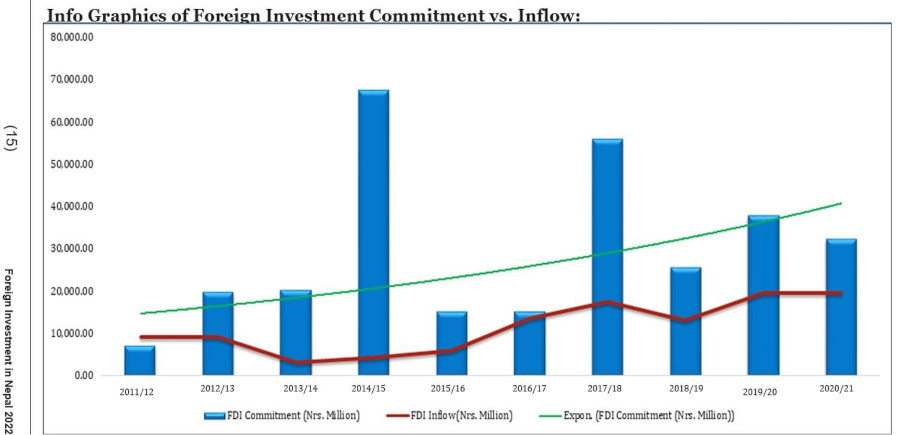

Statistics suggest that FDI flow to Nepal in 2021 and 2022 has rebounded and has surpassed pre-COVID levels. While there is a growing sense of optimism with respect to the policy changes and updating of laws related to FDI, it is ‘too little too late’ to kick-start the economy. This is because the small amount of FDI inflow started only in the late 1990s and was severely punctuated by the decade-long Maoist violence; it has barely picked up now to cross 0.5% of the GDP (lower than Maldives, Pakistan, Sri Lanka and certainly India). Another pressing issue has been the gap between the amount of FDI committed by different countries and the actual amount realized as shown in the figure below.

Source: Department of Industries (DoI), 2022

Important to note in the latest DoI report that some of the sectors such as primary agro- production (poultry, fishery, bee-keeping etc), small and cottage industries, and personal services businesses such as tailoring driving, hair salon are kept under the restricted list for FDI. However, Nepal is open for FDI in areas such as agriculture, tourism, energy, manufacturing, and construction which possess huge possibilities of attracting FDI in large volumes and chunks.[10]

This paper explores legal, institutional, structural, and operational aspects that have hindered the inflow of FDI into Nepal.

Nations adopt various means for rapid economic growth depending on their geopolitical location, availability of resources, skilled manpower, infrastructure, and market access. The FDI is one of most important means among them. It brings both funds and technology. FDI is taken as an important source to meet the financing gap and plays a significant role in rapid economic growth for the least developing countries which are mostly seen as technologically and financially poor in utilizing their available resources for economic growth. The opportunities reduce further in the case of a landlocked country and its economic dependence on its neighbours like Nepal. Despite adopting advanced economic policies and periodical reforms to attract foreign investments since the 1990s, Nepal has been perennially unsuccessful in attracting foreign investors.

Nepal aims to become a middle-income country and achieve the Sustainable Development Goals by 2030. According to a World Bank report, the current level of foreign investment is not enough for the country to transit to the middle-income stage from its current low-income status.

As per the 2022-report of the Department of Industries,[11] Nepal has several foreign investment- related acts and regulations in place to ensure enabling environment in order to attract and mobilize foreign capital and technology investment (see annexure-1).

The new investment-friendly policies adopted by Nepal have guided the policy makers to go for four institutional arrangements (see annexure-2) for administration and implementation of rules and regulations related to FDI. The Investment Board Nepal (IBN) is mainly responsible for the approval of FDI projects greater than or equal to NPR 06 billion and at the same time approval and implementation of energy projects with the capacity greater than or equal to 200 megawatts. The DoI provides the services for approval of foreign investment not exceeding NPRs. 6 billion. Ministry of Industry, Commerce and Supplies oversees policies, laws, criteria, planning implementation, and regulation regarding foreign investment and technology transfer and also those issues related to patent, design, trademark, geographical indication, etc. The Foreign Exchange Facilitation Unit of Nepal Rastra Bank (NRB) has an important role to play such as providing approval to remit foreign currency into Nepal as foreign investment or as foreign loan, recording FDI and providing repatriation facilities among others.

The undermentioned top-10 sectors are identified on the basis of high returns and less risk averse.

Even after making these arrangements, contentious issues still persist involving the exit process, repatriation, lack of law with respect to digital FDI, etc. There are several reasons for the continued poor FDI inflow and non-realization of the investment potential in Nepal. Some of the important constraints are identified below:

Political system and future trends

There is a strong correlation between ‘political stability’ and ‘steady economic growth’. Although both these elements complement each other, a strong political system and visionary leadership often help in projecting a country’s domestic market as dependable for outsiders. In the case of Nepal, the Himalayan country has been visited by chronic political instability and absence of visionary leaders, which have contributed to the low confidence level of investors.

As has been noted above, FDI inflow into Nepal has never been impressive despite the fact that domestic market was opened to foreign investors in 1984. The political change of 1990 that led to end of absolute monarchy and beginning of constitutional monarchy after a successful Jan Andolan (Peoples’ Movement), at least in theory, accelerated the process of economic reforms, and brought about changes in legal, structural, institutional and operational levels, which were partly designed to attract more FDI in the economy. But even after these initiatives, average flow of FDI (2000-2022) continues to hover around 0.27 % of the national GDP on an average. FDI as percent of nominal GDP has never crossed 0.5% range, except in 2010, 2019, and 2021.[12] Since the onset of democracy in the 1990s, Nepal has seen 27 Prime Ministers, which means that on an average, Nepal has had one PM per year (as on 25 November 2022).

In the post-Constitution period, since 2015, there has not been a major improvement in the political situation in Nepal. In the last seven years, Nepal has seen five Prime Ministers (October 2015-November 2022) and there have been two attempts to dissolve the House of Representatives (HoR) pre-maturely which has led to loss of popular confidence in the new political system. The recurring political instability has had a heavy toll on the country’s economy, and governance and deepened the social fault lines in Nepal. The frequent changes in government and unholy alliances among political parties for coming to power at all costs have halted the pace of economic growth. The leaders of Nepal have failed miserably in providing political direction to the institutions for effective implementation of policies.

Nepal is likely to pass through perennial political instability in the future because of the following factors: undemocratic party structures, intra-party factionalism, opportunistic alliances between political parties on the basis of individual interest, nepotism and favoritism in the political parties to select the candidates during elections, domination of the upper castes in Nepalese politics, abnormally high ratio of registered political parties per population, weak electoral governance, and external influence in the internal matters of major political parties.

For example, the government opened the ‘One Stop Service Centre’ in May 2019 to make it easy for investors to receive waivers, facilities and subsidies, and essential infrastructure. But the implementation of the policies has not been so consistent due to the prevailing instability in the system.

Other than political instability, Nepal is also prone to domestic political unrests occasioned by regular protests by the marginalized groups, call for political and economic shut down by the radical left outfits, strikes called by right-wing political parties for revival of Monarchy in Nepal, communal and ethnic violence in the Terai region, etc. During the 10-years of Maoists insurgency, a large number of foreign investors withdrew their investments citing the following reasons: an insecure market situation due to forced donations, trade union strikes, and Maoists- motivated protests by the locals in remote areas. Although the Maoists were politically mainstreamed in 2008, the culture of strikes and forced donations continues in remote areas by some of the recalcitrant left-radical groups. Moreover, sometimes, the Janajatis express their anger over development projects because they perceive such interventions as posing threats to their culture and ancestral land rights and their rights over natural resources under the ILO Convention 169 on Indigenous and Tribal Peoples to which Nepal is a signatory.

Most importantly, there has been a disconnect between domestic aspirations, economic/development necessities, and the foreign policy of Nepal given the ideological allegiance of major political parties towards external powers. Once a party is elected to power, its top leaders (especially prime ministerial candidates) devote maximum time to internal power management and pandering to the sensitivities of external powers for personal political security. In that situation, both domestic and external investors lose confidence in the market from the point of view of their long-term interests. This could be the reason why Nepal receives more annual aid than FDI. According to the Ministry of Finance, Nepal received an NPR 86.41 billion in foreign aid commitment in the first quarter (mid-June-October) of 2022. Of that, there is a subsidy of 6.71 billion while NPR79.70 billion is in debt. The share of grants in total foreign aid is 7.77 percent. The share of loans is 92.23 percent.[13]

Currently, foreign businesses continue to interact with bureaucrats at the central government level. With federalism in place, in the long term this might change as provincial governments become fully operational.[14] This might pose additional hurdles as sub-national units are not allowed to pitch for potential FDI projects without prior approval of federal government, which would be further complicated in case of two separate political parties rule at the federal and provincial levels.

Poor Macro-Economic indicators

Over the last three decades (1990-2021), Nepal’s economic growth has remained at an annual average of 4.38% despite the adoption of the liberal economic policies.[15] One of the constraining factors in achieving the aspired level of growth targets set by the National Periodic Plans and the annual budgets has been the unavailability of adequate financial resources forpublic investment and relatively low level of private investment including the Foreign Direct Investment (FDI).

In addition, the capital expenditure allocation of the government is entirely dependent on the foreign financial support in the form of grants, loans and technical assistance. Likewise, the revenue generated in the economy has barely been enough to meet the current expenditure. Evidently, Nepal suffers from chronic low level of investment in the much-needed infrastructure, connectivity, health, education, and social security sectors. The alternatives left to generate the financial resources to invest in these sectors must come from private financing, both from domestic and foreign sources.

The National five year plan, 2019-20, observed that despite the potential and promise as stated above, some of the existing bottlenecks towards attracting FDI are identified such as: frequent revision of laws related to FDI, inadequate development of industrial infrastructure, difficulty in providing security, support services, and incentives, due to the scattered distribution of industries, lack of adequate skilled manpower, lack of research and development activities on industry and market, lack of inter-agency and policy coordination due to the high number of agencies related to investment, inadequate marketing in the international financial market, and lack of bilateral investment protection agreement with prospective source countries for investment (National Five Year Plan, 2019/20-2023/24)[16].

Nepal has signed Bilateral Investment Promotion and Protection Agreement (BIPPA) with six countries starting with France in the year 1983, followed by Germany, UK, Mauritius, Finland and India (in 2011) (NRB, 2018). However, nothing significant has materialized in terms of securing foreign investors even after signing such agreements.

Another worrisome issue for foreign investors is lack of credible data and reliable statistics. The figures quoted in the report by authorities concerned do not seem to tally and hence lacks credibility. For instance, there is no cumulative figures on FDI by Nepal Rastra Bank (NRB) and DoI. This is likely to affect investors’ confidence.

Private umbrella organizations such as Federation of Nepalese Chambers of Commerce & Industry (FNCCI) and Confederation of Nepalese Industries (CNI) are of the view that Nepal lacks friendly business environment because of cumbersome and lengthy processes required to approve any investment proposal, and register businesses. They believe the ‘one stop service centre’ set up at DoI does not seem to be fully functional.[17]

The simultaneous application of multiple laws in foreign loan investment and issues emanating from them continues to imperil investors. Overlapping legislations, among others, also continues to act as a constraining factor that could deter investors from evincing interest in Nepal as a favoured destination.

Besides these, the laws related to Intellectual Property are yet to be amended. Likewise, while Patent, Design and Trademark Act 2022 is in place, the copyright Act of 2002 is archaic and needs amendment. In addition, the bill related to Intellectual Property Right 2019 is yet to be ratified by the parliament. It is time Nepal should pass laws to progressively open the capital market to foreign institutional investors rather than limiting it to accepting venture capital funds alone.

Some legal experts found that in FITTA 2019 while technology transfer and lease have been classified as investment, foreign loan has been removed and now being treated separately. The rationale for change has not been explained. Notwithstanding these legislations and amendments, Nepal has failed to give a crystal-clear message to the investors that its overall investment climate has improved.

Despite a number of laws and policy pronouncements have been put in place in paper to facilitate foreign investment and ameliorate the hurdles faced by investors, these are barely implemented or translated to action. ‘One window’ policy[18] has not been effectively implemented although DoI claims to have it in place.[19]

In addition, inefficiency related to the system, attitude of corrupt officials, bureaucratic mind- set, software issues, add to institutional inefficiency which erode the confidence of the investors. Foreign investors are confused as to which institutions they need to refer to for consultations and suggestions as overlapping laws leave the investors confused. Although Nepal Trade Information Portal[20] has been there for a long time and provides useful information on exports and imports. However, it is neither updated nor does it provide specific information on goods that have export potential and comparative advantage; as a result, foreign investors do not get the right set of information regarding investment and re-investment.

While the service charter of foreign investment and technology transfer section of DoI mentions seven (7) days for new FDI approval, it does not seem to be actually happening in reality. Investors are found to be waiting for a longer period of time, 30 days to a year and half just to get approval for it. Delay is due to reasons such as inactive automatic route and lack of use of electronic means and automated system.[21]

Although the Economic Survey 2020/21 claims that reforms are being made in legal, structural and procedural areas and continues to remain so to further facilitate business operations and improve the business environment, ease in doing business index has not improved significantly. This is because Nepal till date lacks enabling physical infrastructure and technology to support foreign business ventures.

Private actors worry about security risks faced by large hydropower projects located in secluded areas of the country. Risk return ratio is another concern for investors. Nepal’s current rate of return on investment is around 12%. International private investors maintain that this rate must be of at least 16% for a substantial amount of FDI to enter the country (Wagle, 2019).[22]

As of 2022, Nepal barely has its sovereign credit rating[23] though it hurriedly attempted to get one just before the investment summit. There are no mechanisms in place for any carrying out rating and evaluate the credit worthiness of the ventures. Therefore, forex risk and sovereign credit rating are of major concerns to foreign investors.[24]

There are poor operational mechanisms that support digital business. Since policies governing digital FDI and green FDI are not in place, the operation of such e-businesses or green ventures are likely to more challenging as Nepal lacks human resources who can understand the nitty- gritty of such digitally enabled enterprises or green businesses.

Apart from these challenges, there are some other contentious issues that have been either directly or indirectly creating hurdles in the smooth inflow of FDI in Nepal. Those issues are identified below.

1. Despite adequate policies including the FITTA and the introduction of a single window system, multiple agencies are involved in approving FDI. That makes the process time- consuming and costly. Although the online registration system option is available, it asks for hard copies. It is often seen that many ministries are involved in one sector and bring out separate reports. The best example is water resources. Over four Nepali ministries produce separate annual reports on this issue. It is difficult to identify the nodal ministry for this sector.

2. Tax administration has a problem with regard to the precise amount that needs to be paid. Software hassles and bribery are some of the other issues that continue to plague investors.

3. It has mainly appeared difficult to acquire land to set up both industrial and infrastructure projects. For example, the farmers and locals do not allow the setting up of transmission lines on agricultural land. In that case, power evacuation from the generating station has often been difficult due to issues related to compensation and rehabilitation policy for the locals affected by the mega projects. Given the previous experiences, the affected people do not trust the administration due to poor implementation records and also in the absence of attractive compensation and rehabilitation policy for the locals affected by the mega projects. Political and administrative tolerance of local resistance to the new projects for not disturbing political vote banks.

4. The issue of industrial security has been resolved lately after the new labour law and Social Security Fund, and the hire and fire policy was incorporated into the labour law. But the issue of raw materials has been a perennial one. Industries producing pharmaceutical, shoes, textile, iron, and other processing industries are dependent on factors of production including raw materials, labor, and finances.

5. A large portion of foreign investments in Nepal comes from tax haven countries. Media reports indicated that some Nepali politicians transfer illegally earned money to these countries and bring such money back as investment capital.

6. Manufacturing sectors receive fewer investments due to lower production costs in neighbouring countries than in Nepal. Therefore, these countries prefer to use Nepal as a market than as an investment destination. In fact, duty-free access to Nepal’s manufacturing products in the USA and EU has hardly appealed to external investors to invest in the manufacturing sectors of Nepal.

Keeping in view the effects of COVID-19 on fluctuating remittance inflows, widening trade deficit, progress in hydro energy cooperation with India (Power Trade Agreement with India in 2014), and depleting foreign exchange, especially after the Ukraine crisis, Nepal undertook certain measures to attract more FDI. In this regard, the Deuba government fine-tuned the following policies:

1. To encourage more investments in the hydro-energy sector, the government allowed private sectors to engage in power trade. The private developers can now sell their electricity in the free market after taking approval from the ministry and the private sector can also obtain a license to trade power in the international market. Earlier, the developers had only one option— selling electricity to the Nepal Electricity Authority (NEA).[25]

2. In an effort to encourage small investors and the small and medium-scale industries in rural Nepal, in October 2022, the government slashed the investment amount minimum by 60 percent to NPR 20 million. In June 2019, over protests from the private sector, the government jacked up the minimum limit for FDI from NPR 5 million to NPR 50 million.

3. As per the June 2022 Budget statement, an arrangement would be made to approve foreign investments of up to NPR 100 million through an automated system in seven days. The remaining procedures for investment approval and operation would take six months. It is yet to be implemented.

4. Nepal lacks strong and effective implementation of intellectual property laws due to which foreign investors hesitate to make investments. The government had pledged to protect intellectual property and copyright of the creators.

5. To prevent misuse of the business visa facility, the Industry Department will recommend a business visa for three months by which time the investor has to submit a certificate of company registration. After the registration certificate has been received, the department will recommend an extension of the business visa for another three months. Within this period, the investor needs to submit proof of having registered at the tax office and opened a bank account. The investor is also required to produce details of the progress of industry registration. If the Industry Department is satisfied with the paperwork, it can recommend another three-months’ extension. After the applicant has submitted all the documents, the visa will be extended by another six months. After six months, additional visa recommendations will be made under FITTA 2019. Investors or their official representatives and their family members will get residential visas if they make an investment of million at one time.[26]

6. FITTA was first introduced in 1981, revised in 1992 and then later revised in 2019. It was further updated in January 2021. Foreign investors in Nepal need to bring 70 percent of their proposed investment before beginning their operations, and the rest in the next two years, according to a new regulation issued under FITTA. The regulation, also says that investors have to transfer the capital they have pledged within a year of their project being approved and will be issued identity cards according to the size of their investment.[27]

Due to the above-mentioned challenges other than low FDI flow, the FDI realization has been poor and does not match the pledges. According to Nepal Rastra Bank, net FDI decreased by 4.9 percent to NPRs18.56 billion in the last fiscal year. In the previous fiscal year, net FDI amounted to NPRs 19.51 billion.[28] Therefore, a complete eco-system that could support foreign ventures seem to be the need of the hour.

1. FDI approval process needs to be simplified by strictly following online registration system and also identify the nodal agency for wider consultation in case of difficulties.

2. Repatriation process appears cumbersome despite amendments the old regulations in January 2021. That needs to be simplified further by reducing multiagency approval process.

3. Need massive digitisation and e-governance for ensuring the process is free form corruption, bottlenecking, non-transparent and easy access to multiple economic data base of Nepal.

4. Nepali missions will have to play a vital role in information dissemination and remain open for initial consultations regarding investment potential and procedures in Nepal. They should hold periodical business promotion programmes in the countries that have the potential to invest in Nepal or provide market access to Nepali products. The embassies should be authorised to issue a preferential investor certificate (provisional) for fast tracking of the proposals. The embassies and meetings at the bilateral level should encourage friendly/partner countries for more investments than annual aid assistance.

5. Nepal needs to diversify its energy sources and reduce dependence on other countries especially during the winters.

6. The FDI especially in ICT projects plummeted as laws are not in place for cyber security and Intellectual Property Rights (IPR).[29] The latest FITTA, 2019 does not contain any provision on digital FDI. There is a need for suitable laws and rules and regulations for this sector.

7. Last but not the least, there should be clarity from the union government regrading role and responsibilities of the provincial governments regrading project implementation, which is a prerequisite for subnational units for pitching and attracting investments. Moreover, there is a need for ensuring stable government and healthy macro-economic indicators to boost investors’ confidence.

1. Foreign Investment and Technology Transfer Act (FITTA) 2019

2. Foreign Exchange (Regulation) Act 1962

3. Investment Board Act 2011

4. Industrial Enterprises Act 2020

5. Company Act 2017

6. Contract Act 2000

7. Arbitration Act 1999

8. Income Tax Act 2002

9. Labor Act 2017

10. Privatization Act 1992

11. Foreign Investment Policy 2015

12. Public-Private Partnership and Investment Act, 2019

13. Nepal Rastra Bank Foreign Investment and Foreign Loan Management by-law, 2021.

1. The Ministry of Industry, Commerce and Supplies.

2. Department of Industries (DoI).

3. Investment Board of Nepal (IBN).

4. Foreign Exchange Facilitation Unit of Nepal Rastra Bank (NRB).

[1] “India’s economy will expand to trillion by 2050, says Adani”, Hindustan Times, 19 November 2022.

[2] “Have energy needs, no cut for coal phase-down: Power minister R K Singh at Idea Exchange”, The Indian Express, 27 November 2022.

[3] Ministry of Power, Government of India. For details see https://powermin.gov.in/en/content/power-sector- glance-all-india (accessed on 30 November 2022).

[4] “Transmission lines being built to export 13,000 MW electricity to India in next five years: Ghising”, my Republica, 09 September 2022, https://myrepublica.nagariknetwork.com/news/transmission-lines-being-built-to- export-13-000-mw-electricity-to-india-in-next-five-years-ghising/ (accessed on 30 November 2022)

[5] Ministry of Industry, Commerce and Supplies, Department of Commerce, Government of Nepal. For details see https://www.doind.gov.np/detail/145 (accessed on 01 December 2022).

[6] Article 51-d (1), The Constitution of Nepal.

[7] Nepal’s trade deficit between 2003–04 and 2019–20 increased by around 13-fold. Most worrisome is the fact that the import-export ratio of the country has skyrocketed. For details see Dadhi Adhikari “Unravelling the current economic situation in Nepal”, Raisina Debate, Observer Research Foundation, 15 June 2022.

[8] “Slump in power use sign of economic woes”, The Kathmandu Post, 26 November 2022, https://kathmandupost.com/money/2022/11/26/slump-in-power-use-sign-of-economic-woes (accessed on 26 November 2022).

[9] Dadhi Adhikari, “Unravelling the current economic situation in Nepal”, Raisina Debates, Observations Research Foundation (ORF), June 15 2022, https://www.orfonline.org/expert-speak/unravelling-the-current-economic-

situation-in-nepal/ (accessed on 26 November 2022).

[10] For Complete list refer Foreign Investment in Nepal by Department of Industries, 2022, https://doind.gov.np/detail/132 (accessed on 01 December 2022).

[11] Foreign Investment in Nepal by Department of Industries, 2022, https://doind.gov.np/detail/132 (accessed on 01 December 2022).

[12] Foreign direct investment, net inflows (% of GDP) – Nepal”, The World Bank/Data, https://data.worldbank.org/indicator/BX.KLT.DINV.WD.GD.ZS?end=2020&locations=NP&start=1990 (accessed on 30 November 2022)

[13] “Nepal receives foreign aid commitment of Rs 86.5 billion in three months”, my Republica, Kathmandu, 12 November 2022, https://myrepublica.nagariknetwork.com/news/nepal-receives-foreign-aid-commitment-of-rs-

86-5-billion-in-three-months/ (accessed on 26 November 2022).

[14] “2021 Investment Climate Statements: Nepal”, US Department of State, https://www.state.gov/reports/2021- investment-climate-statements/nepal/ (accessed on 30 November 2022).

[15] “GDP growth (annual %)”, The World Bank, Data, ttps://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2021&locations=NP&start=1990&view=char t (accessed on 30 November 2022

[16] The Fifteenth Plan (Fiscal Year 2019/20–2023/24), National Planning Commission, Government of Nepal, https://npc.gov.np/images/category/15th_plan_English_Version.pdf (accessed on 30 November 2022).

[17] https://ekantipur.com/business/2022/11/11/166813045113673656.html (vernacular news portal), (accessed on 30 November 2022).

[18] https://nayapatrikadaily.com/news-details/62896/2021-04-18 (Vernacular new portal), (accessed on 30 November 2022).

[19] https://www.himalkhabar.com/news/10826 (Vernacular new portal), (accessed on 30 November 2022).

[20] Trade and Export Promotion Centre, Ministry of Industry, Commerce and Supplies, Government of Nepal, https://nepaltradeportal.gov.np/ (accessed on 30 November 2022).

[21] https://bizmandu.com/content/20221101112808-1.html (accessed on 30 November 2022).

[22] Achyut Wagle, “Nepal’s potential for blended finance: A country-level study,” Occasional Paper Series No-48, Southuthern Voice, January 2019, http://southernvoice.org/wp-content/uploads/2019/04/Ocassional-Paper- Series-N48-final.pdf (accessed on 01 December 2022).

[23] Sneha Shrestha, “Relevance of Sovereign Credit Rating in Nepal”, Nepal Economic Forum, 19 April 2022, https://nepaleconomicforum.org/relevance-of-sovereign-credit-rating-in-nepal/ (accessed on 30 November 2022).

[24] “Currently, forex risks and sovereign credit rating are top concerns of FDI investors” New Business Age, Kathmandu, 16 January 2021, https://www.newbusinessage.com/MagazineArticles/view/2907 (accessed on 30 November 2022).

[25] “Government goes the ordinance way to allow private sector in electricity trade”, The Kathmandu Post, 01 October 2022, https://kathmandupost.com/money/2022/10/01/government-goes-the-ordinance-way-to-allow- private-sector-in-electricity-trade (accessed on 26 November 2022).

[26] “Nepal tightens business visa rules for foreign investors to prevent misuse of the permit” The Kathmandu Post, 05 November 2022, https://kathmandupost.com/money/2022/11/05/nepal-tightens-business-visa-rules-for-

foreign-investors (accessed on 26 November 2022).

[27] “Nepal issues new regulations regarding foreign investment”, The Kathmandu Post, 20 January 2021, https://kathmandupost.com/money/2021/01/20/nepal-issues-new-regulations-regarding-foreign-investment (accessed on 26 November 2022).

[28] “Minimum foreign investment amount cut to Rs20 million”, The Kathmandu Post, 14 October 2022, https://kathmandupost.com/money/2022/10/14/minimum-foreign-investment-amount-slashed-to-rs20-million (accessed on 26 November 2022).

[29] “Potential foreign investors put off by Nepal’s lax law enforcement” The Kathmandu Post, 19 June 2922, https://kathmandupost.com/money/2022/06/19/foreign-investors-put-off-by-nepal-s-lax-law-enforcement (accessed on 30 November 2022).